The Cashless Shift in America: What It Means for Shoppers and Businesses

Uniqode used Pew Research Center survey data to analyze the economic impact of shifting away from the usage of cash among Americans in recent years.

Step aside, cash: There’s a new king in America, and it’s made of plastic.

Fewer Americans are using cash for everyday purchases, favoring credit or debit cards and smartphone wallets instead. Several trends have fueled this shift.

Online shopping has skyrocketed, with online retail sales quadrupling over the past decade. Today, about 15% of U.S. retail sales are made online, according to Census Bureau data. The COVID-19 pandemic accelerated this trend, changing the way Americans shop both online and in-store.

Many retailers stopped accepting cash during the pandemic to reduce germ exposure. A 2021 Square survey found that about 18% of businesses weren’t accepting cash due to the pandemic, with 3% saying they had no plans to accept it again. Retailers, from hardware stores to fast food chains, have also added self-checkout stations for card or mobile payments and reduced the number of cash-only checkout lines.

For consumers, cards and mobile payments are simply more convenient. They make it easier to track spending, manage budgets, and replace lost or stolen cards (something cash can’t do). However, millions of Americans don’t have bank accounts, and this shift toward a cashless economy could leave them behind.

Uniqode analyzed Pew Research Center survey data to highlight how Americans are shifting away from cash and how this trend impacts companies and consumers.

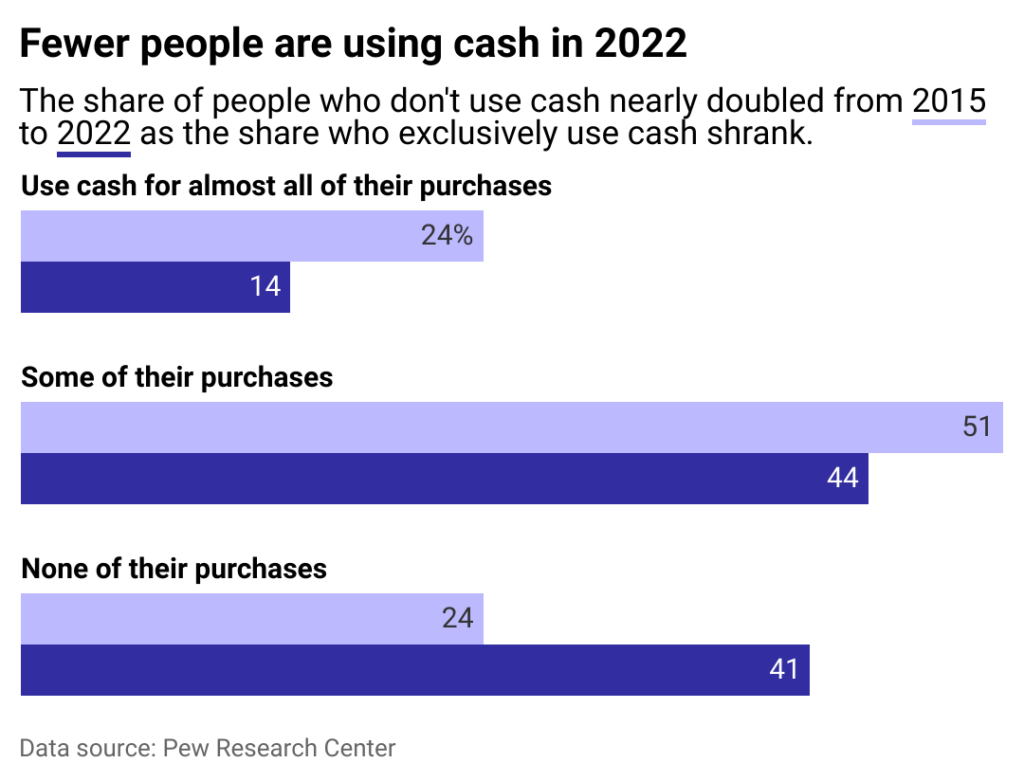

About 2 in 5 Americans are exclusively making cashless purchases

The U.S. is moving towards a cashless society. Pew Research Center survey data shows that about 2 in 5 people in the U.S. don’t use cash for any of their typical purchases, a sharp increase from 2015.

Meanwhile, the share of people who use cash for all or some of their purchases has dropped. Still, about 3 in 5 Americans try to keep cash on hand, whether or not they will use it.

Disparities in cash usage

Cash usage is not evenly distributed. Black, Hispanic, and lower-income Americans are more likely to rely on cash to pay for some or all of their purchases. While just 14% of all Americans say they use cash on nearly all of their purchases, that figure reaches 30% among households earning under $30,000 annually. Additionally, 26% of Black adults and 21% of Hispanic adults pay for most things with cash.

These disparities, based on race, ethnicity, and socioeconomic status, have important implications for a cashless economy. Populations that rely heavily on cash are also more likely to be unbanked or underbanked. “Unbanked” refers to people without a checking or savings account, while “underbanked” describes those who have a bank account but rely on alternatives like money orders, check-cashing services, or payday loans, often carrying extra fees or interest. In recent years, one option that has grown in adoption especially among small businesses and digital-first operators is the use of a cash management account. These accounts combine basic banking functions with simplified cash flow handling, offering a low-fee structure and online accessibility that can reduce reliance on high-cost financial alternatives

Unbanked households risk getting left behind as the cashless economy grows

According to the Federal Deposit Insurance Corp.’s (FDIC) data, 4.5% of U.S. households were unbanked in 2021, and another 14.1% were underbanked. Cash remains essential for these groups, which also include people with lower education levels, those with disabilities, and single-mother households.

While the share of U.S. residents without bank accounts is shrinking, the rise of cashless businesses poses challenges for the unbanked. Most stores that have phased out cash are unlikely to reverse course, as reducing cash payments speeds up transactions and cuts labor needed for cash handling.

To help those who want to participate in cashless purchasing, federal and state programs, such as the FDIC’s Money Smart program, encourage and support creating bank accounts.

Lacking funds was the primary reason for being unbanked. But about 13% of unbanked households said they don’t trust banks, and another 8% believe that not banking gives them more privacy. This means that for the cashless economy to grow inclusively, government efforts must include low-balance banking options and financial education, helping people safely engage with financial institutions while protecting their personal data.

Cash may no longer be king, but its decline leaves a clear challenge: ensuring no one is shut out of the economy. For businesses, cashless payments mean speed and efficiency. For consumers, they bring convenience and security. The future of money in America will depend on finding the balance between progress and inclusion.

Story editing by Elena Cox. Copy editing by Tim Bruns.